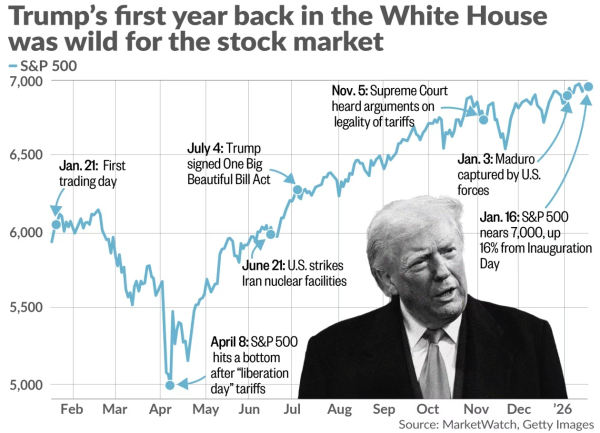

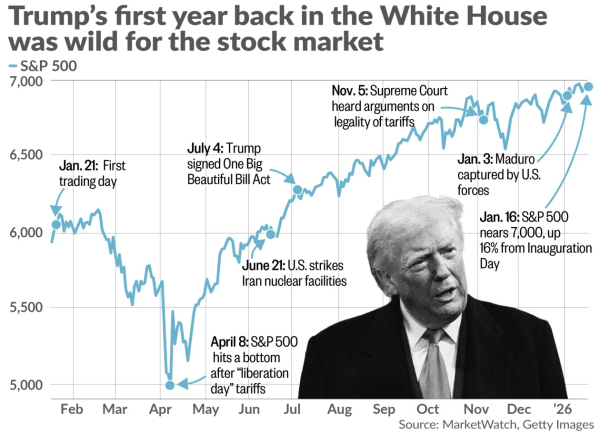

Following his return to office on January 20, 2025, the S&P 500 benchmark has increased by almost 16% , despite substantial fluctuations and various abrupt pullbacks throughout the year.

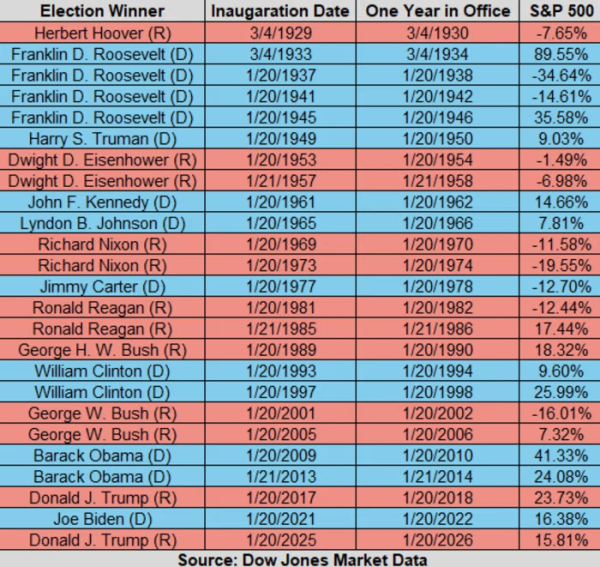

Although this is noteworthy, it isn’t extraordinary when considering past performance. As per Dow Jones Market Data, the typical gain for the S&P 500 during the inaugural year of a presidential administration since 1929 is approximately 9% . As a point of reference, during the initial year of Joe Biden’s term as president, the index expanded by 16.4%, and back in 2017—during the first year of Trump’s earlier mandate—the market gained 23.7%. The market displayed even more vigorous movement in the debut years of Barack Obama’s tenure.

Instability, levies, and “purchasing on dips”

Trump’s initial year in power has featured significant market variations, fluctuating between record peaks and brief downturns. Since the declaration of the so-called “Liberation Day levies” in April, nearly every period of decline has been followed by intense stock acquisitions by investors.

This pattern has colloquially become known as the “TACO trade” within Wall Street circles and has underlined a crucial insight from 2025: that prominent governmental choices don’t invariably result in enduring adverse market outcomes . Simultaneously, experts caution that such a method might diminish investors’ awareness of emerging risk sources in 2026.

Index milestones and macroeconomic context

Since Trump’s return to the Executive Branch , the S&P 500 has attained new pinnacles 42 times , the Dow Jones Industrial Average 23 times, and the Nasdaq Composite has concluded trading at record highs on 36 occasions.

The US financial system has generally expanded more rapidly than projected. Subsequent to a GDP contraction in the initial quarter of 2025, the economy has rebounded throughout the subsequent two quarters, and US GDP escalation in 2025 is assessed to be 2.5% or greater . The rate of joblessness was 4.4% in December, hovering close to a two-year low, while the rate of inflation eased to 2.7% when annualized.

Governance, the Central Bank, and the Dangers of 2026

The prevailing financial landscape is being enhanced by the Trump leadership’s economic proposals, notably the One Big Beautiful Bill Act and initiatives aimed at decreasing consumer borrowing expenses. Concurrently, markets are vigilantly observing the Federal Reserve's strategies and the circumstances surrounding its governor , Jerome Powell , which is encouraging deliberations concerning the regulator’s autonomy.

An additional aspect of unpredictability is the Congressional midterm contests in the US come 2026. Historically speaking, the second year of a presidential term is the most anemic for the equity market: since 1948, the average yield of the S&P 500 in midterm polling years has barely reached 4.6%.

The outset of 2026: a shaky introduction

The initial weeks of 2026 have already signaled heightened market strain amid geopolitical risks, spanning from military occurrences in Venezuela to intensifying animosity between the US and Iran. In the past week , the Dow Jones contracted by 0.3%, the S&P 500 dipped by 0.4%, and the Nasdaq slipped by 0.7% .

In conclusion, Trump’s reconvening to the White House yielded considerable appreciation for investors , while simultaneously establishing the conditions for a more challenging and erratic 2026.